Britain’s Rentier Economy Is Why a Coffee Now Costs £5

by Jaffa Levy

·

Published

· Updated

The rise of the £5 coffee is not about wages or beans. It is about how Britain chose to organise its economy, and who it chose to reward.

The £5 coffee is not about beans or baristas. It is the visible price of how Britain organised its economy.

I am sitting in Fitzrovia, just off Marylebone High Street, in a small independent cafe. The room is narrow, unremarkable, quietly busy. I order a latte. It costs £4. When I ask, almost casually, I am told it will soon be £5.

This is no longer unusual. Five pounds for a basic coffee is becoming normal across London and other large British cities. The BBC and others report it as a story about rising wages, energy costs, and global coffee prices.

That explanation is incomplete.

The more important question is not why coffee is more expensive, but what we are really paying for.

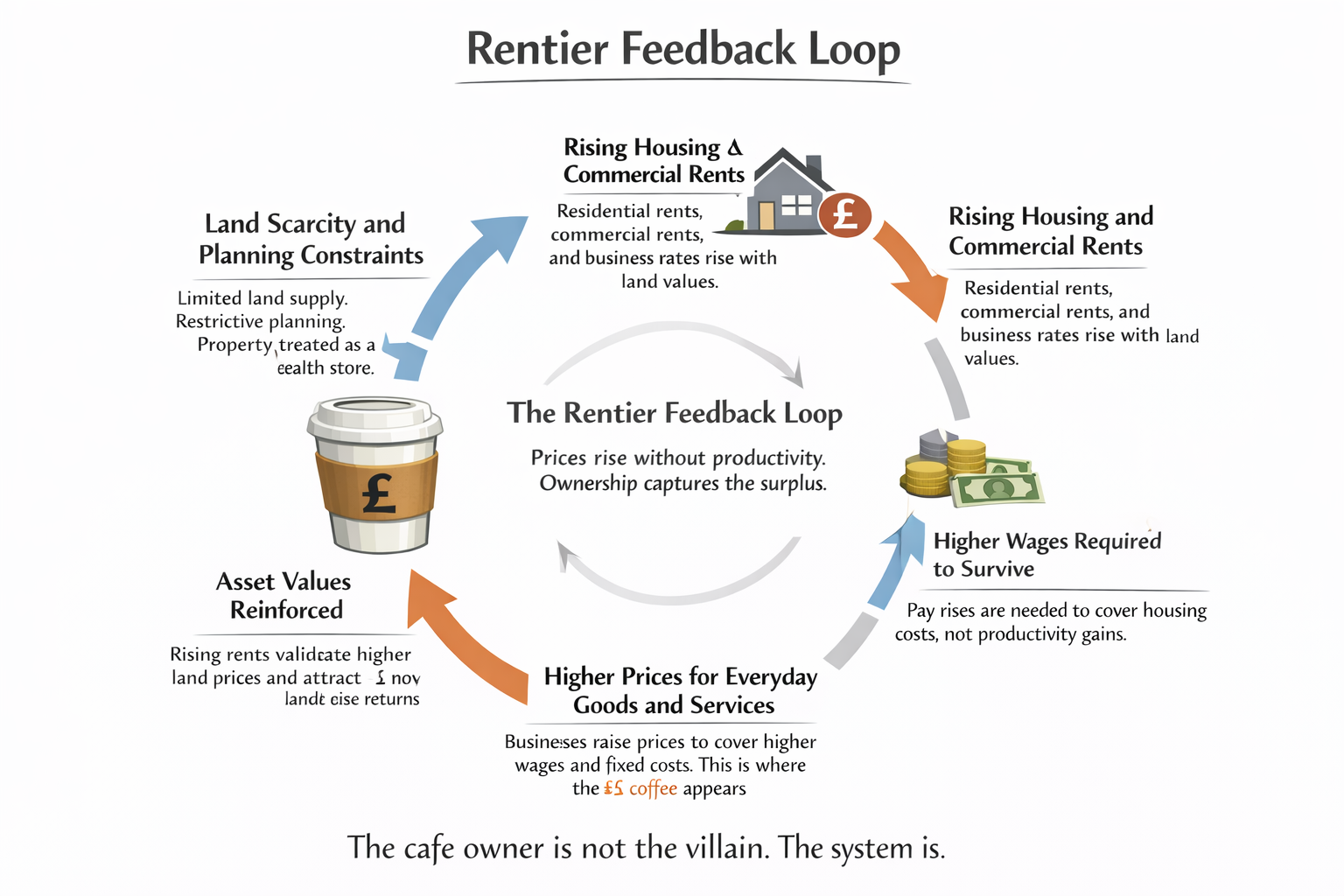

This is not a story about coffee. It is a small, everyday example of how a rentier economy works.

A rentier economy is one where income and prices are increasingly determined not by production, but by ownership of scarce assets. Land, housing, commercial property, and the financial claims tied to them become the primary sources of return. Those who control access are rewarded. Those who produce pass the toll.

The beneficiaries are concentrated:

Residential landlords

Commercial property owners

Landowners in constrained urban areas

Financial institutions whose profits depend on rising asset values

They do not make the coffee. They do not improve productivity. They earn more because scarcity is protected and monetised.

The coffee itself has not become rare. Beans are globally traded. Machines are standardised. Milk, water, electricity and labour costs have risen, but nowhere near in proportion to the retail price. Strip the drink back to its essentials and it is recognisably the same product in many countries.

The price difference sits outside the cup.

Retail price per cup

London (central cafe): £4.00

Ho Chi Minh City: £1.50 to £1.85

Ingredients do not explain the gap.

Ingredient cost per cup

Britain: £0.45 to £0.55

Vietnam: £0.30 to £0.40

The difference appears in rent, labour, tax and compliance. But the crucial issue is why those costs behave as they do.

Labour is expensive in London because living in London is expensive. Wages rise to cover housing costs. Housing costs rise because land is scarce, planning restricts supply, credit inflates prices, and property is treated as a primary store of wealth. Higher rents force higher wages. Higher wages are then blamed for higher prices.

Much of the money flows straight through.

This is the rentier feedback loop in miniature.

The £5 coffee appears as an outcome, not a cause.

Despite higher prices, British cafe owners often retain thin margins.

Estimated net profit per cup

Britain: £0.20 to £0.40

Vietnam: £0.30 to £0.60

The system extracts surplus before the business sees it.

Vietnam is not offered as a romantic comparison. It is a control. A predictable objection follows: Vietnam is poorer.

So remove poverty from the explanation.

Germany is a rich, high-wage economy using the same machines, beans and global supply chains. If wages alone explained British prices, Germany should look similar.

It does not.

Retail price per cup

London: £4.00

Berlin or Munich: £2.20 to £2.80

The difference is structural.

Germany constrains land and housing differently. Rents are anchored by transparent local indices. Long tenancies are normal. Its decentralised banking system directs credit toward productive investment rather than urban land speculation. Asset inflation is not treated as a national growth strategy.

As a result, everyday services remain cheaper in a rich economy.

Britain made a different set of choices.

Housing was financialised. Land scarcity was protected. Asset appreciation was encouraged. Transactions were taxed more heavily than rents. Ownership was rewarded. Access was priced.

The £5 latte is not an anomaly. It is evidence.

Rentier economies feel busy but grow slowly. Investment flows into existing assets rather than new capacity. Prices rise faster than living standards. The economy looks active, yet value drains upward through ordinary transactions.

This outcome is not inevitable. It is the result of policy.

The real question is not whether Britain can afford a five-pound coffee. It can.

The question is what kind of economy produces one, and who that economy is designed to serve.

A rentier economy is not complicated. Income flows to those who control access, not to those who produce. Scarce assets are owned by a relatively small group. Returns are protected by law, planning, credit allocation and tax design. Work carries the risk. Ownership collects the return.

As scarcity deepens, rents rise. As rents rise, wages rise just to survive. Prices then rise to cover wages. The cycle feeds itself. Meanwhile, rentier income is often taxed more lightly than work or consumption.

The £5 coffee is not about coffee. It is what a rentier economy looks like when it reaches the street.

Another article on the rentier economy on Telegraph.com